IFRS 9 Financial Instruments Reporting COVID-19 Impact

IFRS 9 financial instruments reporting coronavirus pandemic examines how the global health crisis reshaped financial reporting practices. The pandemic’s economic fallout significantly impacted the credit quality of assets, forcing companies to adapt their impairment assessments and reporting strategies under IFRS 9. This analysis delves into the specific challenges, adjustments, and reporting practices adopted by businesses during this period.

This detailed look at IFRS 9 and the coronavirus pandemic will explore the implications for various financial instruments, considering specific industries and the overall impact on financial statements. We will examine the key provisions of IFRS 9, its impairment models, and the unique challenges presented by the pandemic.

IFRS 9 Implications for Financial Instruments: Ifrs 9 Financial Instruments Reporting Coronavirus Pandemic

IFRS 9, issued by the International Financial Reporting Standards Foundation, significantly altered how companies report financial instruments. This new standard introduced a more forward-looking approach to recognizing and measuring financial assets, focusing on the economic reality of the instrument rather than just its contractual terms. It requires a more comprehensive assessment of the potential for losses, reflecting a more cautious approach to financial reporting.IFRS 9 aims to improve the relevance and reliability of financial reporting by requiring companies to recognize expected credit losses (ECL) on financial assets.

This approach recognizes that credit risk is inherent in many financial instruments, and by proactively accounting for potential losses, the financial statements provide a more accurate picture of the company’s financial health. This enhanced disclosure allows investors and stakeholders to make more informed decisions.

Key Provisions of IFRS 9

IFRS 9 Artikels a comprehensive framework for recognizing and measuring financial instruments. Crucially, it mandates a significant shift towards a more forward-looking approach, emphasizing the probable future credit losses rather than just the losses that have already occurred. This proactive approach to recognizing expected credit losses reflects the inherent uncertainties in financial instruments and provides a more realistic assessment of their value.

Impairment Models under IFRS 9

IFRS 9 introduces three different impairment models for financial assets, each based on the credit risk inherent in the asset. These models aim to provide a more accurate representation of the financial instrument’s value, reflecting the potential for future losses.

- Stage 1: This stage applies to financial assets with low credit risk. It involves recognizing expected credit losses (ECL) based on the current conditions of the asset, reflecting the credit risk of the instrument as of the reporting date. For example, a loan to a customer with a strong credit history would likely be categorized in this stage.

- Stage 2: This stage applies to financial assets with moderate credit risk. It requires recognizing ECL based on the historical loss experience, the current economic conditions, and the asset’s current status. Consider a loan to a customer experiencing financial difficulty, but not yet in default. The ECL would be calculated using a combination of historical data and the current economic outlook.

- Stage 3: This stage applies to financial assets with significant credit risk. It mandates recognizing the full expected credit loss, essentially recognizing the full loss that is expected to be incurred on the instrument. This might include loans to customers in default or near default, as the probability of loss is high.

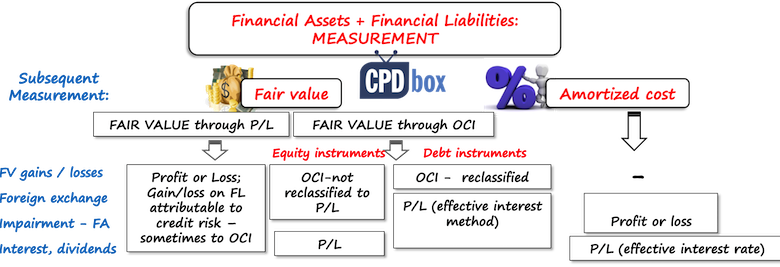

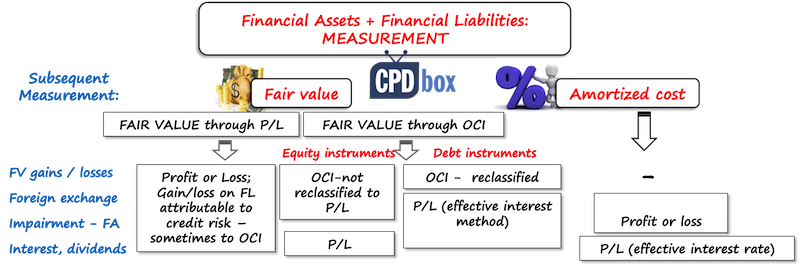

Impact on Classification and Measurement of Financial Assets

IFRS 9 significantly impacts the classification and measurement of financial assets. The standard requires companies to classify financial assets into different categories based on their contractual cash flow characteristics and the business model for managing those assets. The choice of classification impacts the measurement model applied to the asset.

Comparison with Other Accounting Standards

Previous accounting standards, such as IAS 39, often used a simpler approach to measuring credit losses. IFRS 9, by contrast, is more sophisticated, requiring a more forward-looking approach to recognizing expected credit losses. This difference reflects the evolving understanding of credit risk and the desire for a more accurate representation of the potential losses inherent in financial instruments. For example, IAS 39 often relied more on the historical loss experience, whereas IFRS 9 emphasizes the current economic conditions and the instrument’s current status.

Categories and Measurement Models

The following table Artikels the different categories of financial assets and their corresponding measurement models under IFRS 9.

| Category | Measurement Model |

|---|---|

| Amortized Cost | Used for financial assets with contractual cash flows that are solely payments of principal and interest and where the business model is to hold the asset to collect contractual cash flows. |

| Fair Value Through Profit or Loss | Used for financial assets held for trading and those designated as such. |

| Fair Value Through Other Comprehensive Income | Used for financial assets held for sale and those designated as such, as well as for those where the business model is to collect substantially all of the contractual cash flows. |

Impact of the Coronavirus Pandemic on Financial Instrument Reporting

The COVID-19 pandemic triggered a global economic downturn, significantly impacting the credit quality of financial assets held by businesses and financial institutions. This disruption necessitated a careful review and application of IFRS 9, the International Financial Reporting Standard for financial instruments, to accurately reflect the changing economic realities. Companies had to adapt their financial reporting to account for the potential for increased losses on their financial instruments.The pandemic highlighted the dynamic nature of financial risk assessment.

Traditional models, often relying on historical data, struggled to capture the rapid shifts in economic conditions. Companies had to incorporate external factors, such as government support programs and evolving market trends, into their impairment assessments. This meant a more nuanced approach to understanding and quantifying the potential for loss on financial assets.

Impact on Credit Quality of Financial Assets

The pandemic’s economic fallout led to a sharp decline in economic activity and consumer confidence. This directly impacted the creditworthiness of borrowers across various sectors. Businesses faced reduced revenue streams, increased operating costs, and difficulties in meeting their obligations. The resulting rise in defaults and delinquencies had a significant impact on the credit quality of financial assets held by lenders and investors.

Key Challenges in Applying IFRS 9 During the Pandemic

Companies faced numerous challenges in applying IFRS 9 during the pandemic. The rapid and unpredictable nature of the economic downturn made it difficult to accurately forecast future cash flows and assess the impact on the recoverable amounts of financial assets. The lack of historical data for similar economic events further complicated the process. Furthermore, the availability of reliable information on the specific impact on different sectors and industries was often limited.

This resulted in a higher degree of uncertainty and judgment in applying the standard.

Potential Adjustments to Impairment Assessments

IFRS 9 requires impairment assessments to consider the expected credit losses (ECL) over the life of a financial instrument. The pandemic prompted adjustments to these assessments. Companies needed to incorporate the increased likelihood of defaults and the potential for lower future cash flows. This often meant higher impairment charges than would have been anticipated in normal economic conditions.

The specific adjustments varied depending on the sector and the nature of the financial asset.

Examples of Industry Sectors Impacted by the Pandemic

The aviation industry experienced a significant decline in passenger traffic, leading to substantial losses on loans and receivables from airlines and travel agencies. Similarly, the hospitality sector, including hotels and restaurants, faced decreased revenue and occupancy rates, impacting the credit quality of their financial assets. The retail sector also saw a shift in consumer behavior, with some stores facing increased challenges in meeting debt obligations.

Impairment Loss Variations Across Sectors

| Industry Sector | Potential Impact on Impairment Losses |

|---|---|

| Aviation | High; significant decline in passenger traffic |

| Hospitality | High; decreased revenue and occupancy |

| Retail | Moderate to High; shift in consumer behavior |

| Manufacturing | Moderate; varied impact depending on supply chain disruptions |

| Energy | Low; stable demand and government support |

The table above provides a simplified illustration of the potential impact on impairment losses. The actual variation across sectors would depend on a multitude of factors, including specific business strategies, financial leverage, and access to government support programs.

Reporting Practices During the Pandemic

The COVID-19 pandemic significantly impacted financial markets and business operations worldwide. This disruption necessitated adjustments in financial instrument reporting practices. Companies needed to adapt their methodologies to reflect the unprecedented economic uncertainty and volatility. Understanding these adaptations is crucial for evaluating the accuracy and reliability of financial statements during this period.

Common Reporting Practices

Many companies adopted more conservative impairment assessments for financial assets, reflecting the heightened risk of default or decreased value due to the pandemic. This conservatism aimed to provide a more realistic picture of the financial position and potential losses.

- Increased frequency of impairment reviews: Companies recognized the need to more frequently evaluate the fair value of financial assets and reassess impairment allowances to account for the rapidly evolving economic climate.

- Emphasis on qualitative disclosures: Recognizing the limitations of quantitative data alone, companies often included detailed qualitative explanations in their financial statements to elaborate on the factors impacting impairment assessments, such as industry-specific downturns, supply chain disruptions, and government support programs.

- Utilization of scenario analysis: To gauge the potential impact of various pandemic-related scenarios on the value of financial assets, companies incorporated scenario analysis into their impairment assessments. This involved modelling different economic outcomes, considering the various uncertainties associated with the pandemic.

Examples of Modified Impairment Assessments

Several companies adjusted their impairment assessments based on the specific circumstances of their industries and exposure to pandemic-related risks. For instance, airlines, hospitality companies, and retailers experienced substantial revenue declines, leading to higher impairment charges on loans and receivables.

- A bank with significant exposure to small businesses in the restaurant industry might have observed a higher default rate and reduced future cash flows. Consequently, they might have increased impairment provisions for these loans.

- A consumer finance company facing a surge in delinquencies on auto loans due to job losses could have revised its impairment calculations upward to account for the potential for higher losses.

Comparison of Impairment Calculations, Ifrs 9 financial instruments reporting coronavirus pandemic

| Characteristic | Impairment Calculation (Pre-Pandemic) | Impairment Calculation (Post-Pandemic) |

|---|---|---|

| Economic Outlook | Based on historical trends and established economic models. | Considered the unprecedented uncertainty and volatility of the pandemic; utilized scenario analysis and qualitative disclosures. |

| Input Data | Relied primarily on historical data, market conditions, and credit ratings. | Incorporated alternative data sources, including industry-specific data, expert opinions, and government reports. |

| Frequency of Assessment | Usually conducted on a periodic basis, often quarterly or annually. | Increased frequency to capture the dynamic nature of the pandemic and its impact on financial instruments. |

| Qualitative Disclosures | Limited qualitative explanations. | Comprehensive qualitative disclosures to justify adjustments and assumptions. |

Importance of Consistent and Transparent Reporting

Maintaining consistent and transparent reporting practices was crucial during the pandemic. Investors and stakeholders needed clear and reliable information to assess the impact of the crisis on companies and make informed decisions. Inconsistencies could have led to misinterpretations of financial performance and potentially inaccurate valuations.

Impact on Historical Data

The pandemic significantly diminished the reliability of historical data in impairment assessments. The unprecedented nature of the crisis made it challenging to predict future behavior based on past patterns. Companies needed to rely more on forward-looking projections and scenario analyses.

IFRS 9 and Financial Instrument Reporting Adjustments

The COVID-19 pandemic significantly impacted global economies, leading to adjustments in various accounting standards, including IFRS 9. This necessitated a nuanced approach to financial instrument reporting, recognizing the unique challenges faced by businesses during this period. The standard’s flexibility and its ability to adapt to evolving economic realities were crucial in ensuring accurate and reliable financial reporting during this period of uncertainty.

IFRS 9, focusing on impairment, expected credit losses, and classification of financial assets, needed adjustments to reflect the economic downturn. The key adjustments centred around the impact of the pandemic on the creditworthiness of borrowers and the need for more cautious estimations of expected credit losses. This required a more dynamic approach to impairment assessments, moving beyond historical data to incorporate the unique economic factors brought about by the pandemic.

Adjustments to IFRS 9 Guidelines

The pandemic prompted adjustments to the IFRS 9 guidelines for expected credit losses (ECL). These adjustments aimed to reflect the increased credit risk inherent in the economic climate. The adjustments often involved utilizing more forward-looking assessments, considering the potential impact of the pandemic on borrowers’ financial health.

Practical Application in Various Scenarios

Businesses faced diverse situations during the pandemic. For example, a company with loans to small businesses experiencing significant revenue declines required a more pessimistic outlook on their ability to repay. This necessitated higher ECL provisions. Conversely, companies with loans to large, stable corporations might have seen a smaller adjustment in ECL calculations. The application of IFRS 9 required a careful evaluation of each scenario, considering the specific circumstances of each borrower and the overall economic conditions.

The critical aspect was the ability to demonstrate a sound rationale for the impairment adjustments.

Accounting Treatments for Financial Assets

The accounting treatments for financial assets impacted by the pandemic varied based on the nature of the asset and the severity of the impact. For example, loans to sectors particularly hard hit, like hospitality or retail, required higher provisions for impairment. A more detailed assessment of individual borrowers’ financial situations was often necessary. The crucial point was to ensure the treatments accurately reflected the expected credit losses in the current economic context.

Impact on Impairment Losses

The pandemic’s impact on impairment losses was significant. Businesses needed to assess the likelihood of borrowers defaulting and adjust their impairment calculations accordingly. A key component was considering the length of the pandemic’s impact and the possibility of long-term economic repercussions. This often led to higher impairment losses than what might have been anticipated under normal circumstances.

The key was to demonstrate that the impairment provisions reflected a reasonable estimate of the potential losses.

Table: Financial Instrument Treatments

| Financial Instrument Type | Specific Treatment Adjustment (Pandemic Impact) |

|---|---|

| Loans to Small Businesses | Increased impairment provisions due to heightened risk of defaults. |

| Loans to Large Corporations | Impairment provisions potentially adjusted less significantly, depending on the specific industry and company performance. |

| Debt Securities | Increased impairment provisions for sectors negatively affected by the pandemic. |

| Leases | Companies might have adjusted lease accounting based on the impact on lessee’s ability to meet obligations, and therefore, potentially increased impairment provisions. |

Illustrative Cases and Scenarios

Navigating the complexities of IFRS 9 during the pandemic required nuanced application, especially considering the unique economic pressures and uncertainties. Companies across various sectors faced varying challenges in assessing and reporting on their financial instruments. This section provides illustrative cases and scenarios, showcasing how different entities applied IFRS 9 principles in response to the pandemic’s impact.

Retail Sector Application of IFRS 9 During the Pandemic

The retail sector experienced significant disruptions during the pandemic, with store closures and shifts in consumer behavior. This led to a reassessment of financial instruments, including inventory valuations, trade receivables, and potentially even lease liabilities. Retailers needed to critically evaluate the impairment of inventory due to decreased demand and potential obsolescence. Furthermore, they had to carefully analyze the collectability of trade receivables, as economic hardship impacted customer ability to pay.

Manufacturing Sector’s Response to IFRS 9 During the Pandemic

Manufacturing companies faced challenges related to supply chain disruptions, reduced demand, and potential labor shortages. These factors affected the valuation of raw materials, work-in-progress, and finished goods. Companies needed to assess the potential for impairment in their inventory and receivables, adapting their reporting practices to reflect these changing circumstances. Additionally, the impact on production schedules and order fulfillment influenced the assessment of contracts and related financial instruments.

Energy Sector and IFRS 9 Implications During the Pandemic

The energy sector experienced fluctuations in commodity prices and reduced demand due to the pandemic. This impacted the valuation of energy contracts, derivatives, and potentially even oil and gas reserves. Companies had to rigorously assess the impairment of these assets, taking into account the potential for sustained low demand. Furthermore, the implications for future cash flows and contractual obligations needed meticulous consideration.

Case Study: ABC Manufacturing Company’s Handling of a Specific Financial Instrument

ABC Manufacturing, a company specializing in automotive parts, had a significant portion of its revenue tied to vehicle production. The pandemic caused substantial disruptions to the automotive industry, resulting in reduced demand for their parts. This prompted ABC Manufacturing to evaluate the impairment of its receivables from major car manufacturers. Using IFRS 9’s impairment model, they performed a detailed analysis of the expected cash flows, considering the reduced production schedules and potential for further delays.

This led to an impairment loss recognized in their financial statements, reflecting the decreased likelihood of collecting the full amount owed.

Impact of the Pandemic on Fair Value Measurements

The pandemic significantly impacted the fair value measurements of financial instruments. Fluctuations in market conditions and the uncertain economic outlook led to greater volatility in the values of certain financial assets and liabilities. For example, the decreased demand for specific retail products impacted the fair value of inventory, as reflected in market pricing adjustments. The fair value of financial instruments like bonds and equities also experienced considerable fluctuations, requiring continuous monitoring and adjustments.

Significance of Management Judgment and Estimations

Management judgment and estimations played a crucial role in financial instrument reporting during the pandemic. The uncertainty and volatility of the situation made it necessary for companies to make assumptions about future economic conditions and the impact on various financial instruments. Companies had to meticulously document their judgments, clearly explaining the rationale behind their estimations, and providing sufficient supporting evidence to ensure transparency and accountability in their financial reporting.

The quality of these judgments and estimations directly influenced the accuracy of the reported financial data.

Qualitative Considerations

Navigating the pandemic’s impact on financial instruments requires a nuanced understanding beyond just the quantitative adjustments. Qualitative aspects, including disclosure requirements and management commentary, become crucial in providing context and transparency. Investors and stakeholders need to understand not only the reported figures but also the underlying reasoning and potential risks associated with these adjustments.The pandemic’s effect on financial instruments is complex, often involving uncertainties and evolving situations.

Clear and comprehensive disclosures in financial statements are vital to reflect the impact of pandemic-related adjustments. This allows for a more informed assessment of the entity’s financial health and future prospects.

Disclosure Requirements and Management Commentary

Comprehensive disclosures are essential to effectively communicate the pandemic’s impact on financial instruments. Management commentary should explain the rationale behind adjustments, the potential future implications, and the assumptions made. This includes a description of the methodologies used to assess impairment and any significant changes in those methodologies.

- Specific disclosures regarding the pandemic’s impact should be included, outlining the criteria used to determine impairment and any subsequent adjustments. This will help stakeholders understand the rationale behind the decisions.

- Detailed explanations of any changes in accounting policies or estimates due to the pandemic should be clearly Artikeld. This demonstrates a commitment to transparency and accountability.

- Management should discuss the inherent uncertainties surrounding the pandemic’s long-term effects on financial instruments, providing context for the reported figures.

Enhancing Transparency in Disclosures

Enhanced transparency can be achieved through detailed disclosures regarding financial instruments impacted by the pandemic. Companies can improve transparency by providing specific examples of how the pandemic affected the valuation of particular instruments. Illustrative examples and scenarios can be helpful.

- Presenting specific examples of how the pandemic impacted the fair value of particular financial instruments can significantly improve understanding. For example, a company holding a significant amount of loans to small businesses might provide examples of specific loans that experienced a significant decline in fair value due to pandemic-related business closures.

- Companies should provide a clear explanation of the assumptions made when assessing the impact of the pandemic on the financial health of the entity. This includes the methodology used to project future cash flows and the key factors considered.

- Illustrative scenarios can highlight potential future impacts, such as the possibility of further economic downturns. This demonstrates foresight and proactive risk management.

Assessing Pandemic Impact on Financial Health

Assessing the impact of the pandemic on an entity’s financial health requires a comprehensive approach that considers various factors. The analysis should incorporate both quantitative and qualitative assessments.

- Consider the severity and duration of the pandemic’s impact on specific industries or sectors. This is critical in evaluating the potential long-term effects.

- Analyze the entity’s dependence on specific industries or sectors vulnerable to the pandemic. Companies heavily reliant on travel or hospitality, for instance, will face a different impact compared to those in technology or healthcare.

- Evaluate the entity’s ability to adapt to the changing economic environment. Flexibility and resilience are key factors to consider.

Impact on IFRS 9 Interpretation

The pandemic has influenced the interpretation of IFRS 9 principles, particularly concerning the impairment of financial assets. Companies have had to adapt their approaches to reflect the unique circumstances of the pandemic.

- The pandemic’s impact on economic conditions has required a re-evaluation of the reasonable and supportable assumptions used in assessing the impairment of financial instruments.

- The increased uncertainty surrounding future cash flows has necessitated adjustments to the impairment assessment methodology. Companies need to be more adaptable in their assessment of the potential impact of the pandemic on cash flows.

- The increased frequency of economic shocks has highlighted the need for proactive risk management strategies, including scenario planning, to account for future uncertainties.

Final Summary

In conclusion, the IFRS 9 financial instruments reporting coronavirus pandemic presented unique challenges for businesses worldwide. Companies had to adapt their reporting practices to reflect the changing economic landscape and the specific impact on their financial instruments. This required careful consideration of impairment models, adjustments to existing guidelines, and transparent disclosure in financial statements. The pandemic highlighted the importance of consistent and transparent reporting, even in times of uncertainty, and the need for adaptable approaches to financial instrument valuation and impairment assessment.