The Rising Threshold of Middle-Class Stability Why San Francisco Families Now Require Over 400,000 Dollars Annually to Live Comfortably

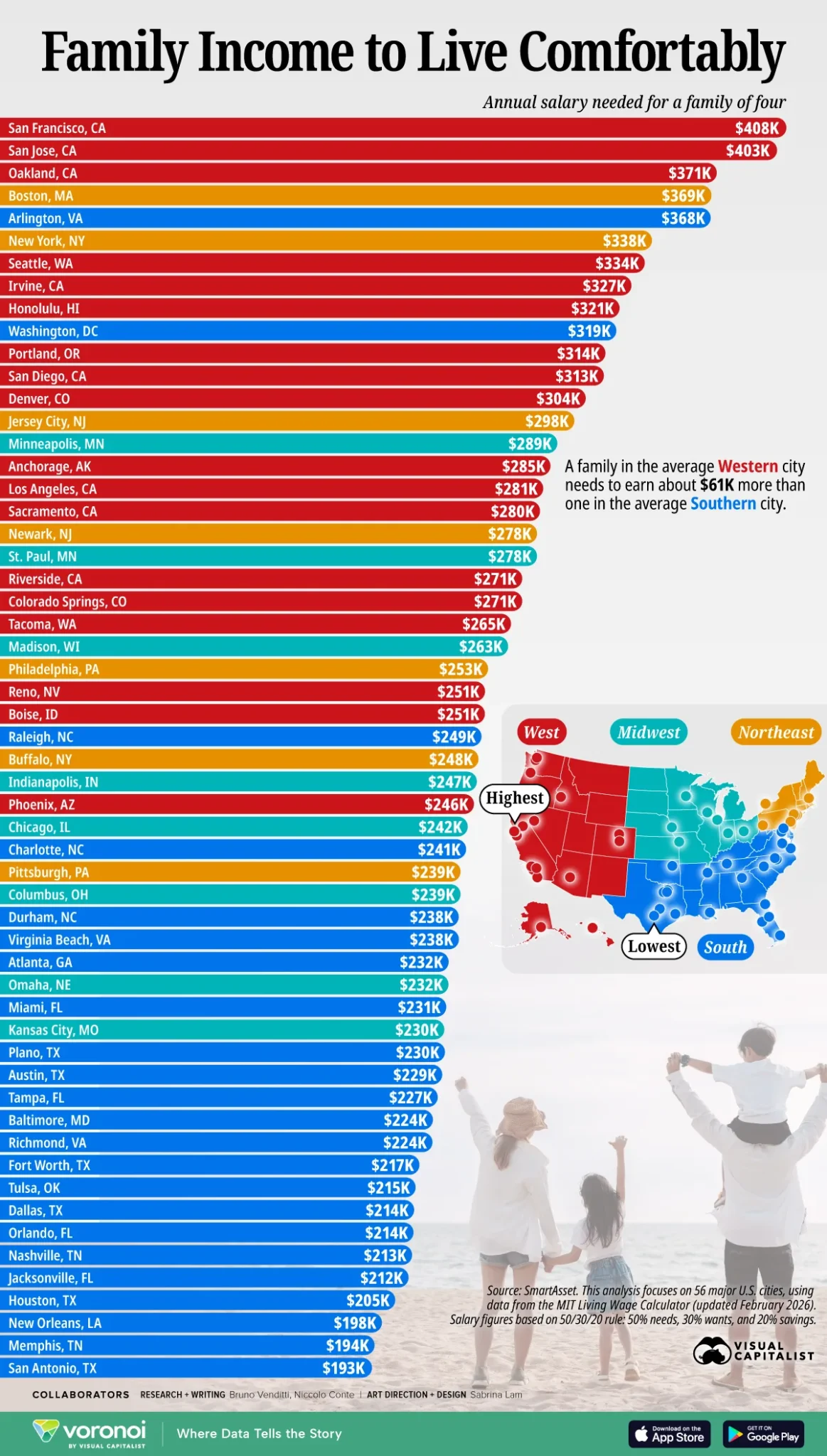

Recent economic assessments of high-cost-of-living urban centers indicate a significant shift in the financial requirements for maintaining a middle-class lifestyle. In San Francisco, a city often cited as the vanguard of American urban affordability challenges, data now suggests that a family of four must earn a gross annual income of approximately $408,000 to live "comfortably." This figure represents a substantial escalation from previous years, reflecting the compounding pressures of inflation, localized housing costs, and the rising price of essential services such as education and healthcare.

The $408,000 benchmark places the required income for a comfortable middle-class existence within the top 5% of household earners in the United States. This trend highlights an intensifying economic phenomenon where a lifestyle historically associated with the median earner—home ownership, reliable transportation, the ability to save for retirement, and providing for children’s education—now necessitates an elite-level income in certain geographic corridors.

The Evolution of Cost-of-Living Projections: A Seven-Year Chronology

The trajectory of middle-class income requirements in coastal hubs has seen a steady upward climb over the past decade. In 2018, initial financial models suggested that $300,000 was the necessary threshold for a family of four in cities like San Francisco or New York. At the time, these estimates were met with considerable public debate, as critics argued the figures were disconnected from the reality of the average American household.

However, subsequent economic shifts necessitated regular revisions to these models. By late 2019, following a period of modest inflation and rising childcare costs, the estimated requirement was adjusted to $350,000. The arrival of the COVID-19 pandemic and the subsequent inflationary spike of 2021–2023 further accelerated these costs. By 2024, and looking toward 2026, the $408,000 figure emerged as the new baseline for a "comfortable" existence.

From a 2017 baseline of $300,000 to the 2026 projection of $408,000, the cost of living for a family of four has increased by roughly 36%. This represents a compound annual growth rate (CAGR) of approximately 3.5%. While this figure is largely in line with broader Consumer Price Index (CPI) trends, it is important to note that the "personal inflation basket" for families in these cities is often weighted toward sectors that outpace general inflation, such as tuition, property taxes, and specialized healthcare.

Deconstructing the 408,000 Dollar Household Budget

To understand how a top-tier income can be rapidly absorbed by the cost of living in a major metropolitan area, it is necessary to examine the post-tax reality and specific line-item expenditures. For a household earning $408,000 in San Francisco, the effective tax rate—combining federal and California state obligations—is approximately 32%. This leaves the household with a net take-home pay of roughly $277,440 per year, or $23,120 per month, prior to any retirement contributions or savings.

Taxation and Fixed Obligations

A significant portion of the gross income—roughly $121,000—is directed toward taxes. While this supports public infrastructure and community services, it reduces the liquidity available for the household’s immediate needs. For families aiming for Financial Independence, Retire Early (FIRE) status, the challenge is amplified. To maintain a lifestyle that costs $280,000 annually in post-tax dollars, a family would need to generate approximately $380,000 in gross passive investment income, assuming a more favorable tax treatment of 26% for dividends and capital gains compared to the 32% rate for W-2 wages.

The Impact of Education and Childcare

Perhaps the most significant variable in the $408,000 budget is the cost of education. In the San Francisco model, approximately $90,000 per year is allocated toward private grade school tuition for two children. While many families opt for public education, those seeking specialized language immersion or specific private curricula find this expense to be a non-negotiable part of their "comfort" definition.

If a family utilizes the public school system, the financial outlook changes dramatically. The $90,000 previously reserved for tuition could be redirected toward 401(k) contributions, taxable investment portfolios, or more aggressive mortgage debt reduction. However, for many high-earning households, the perceived value of private education—particularly in competitive global markets—remains a primary driver of their financial planning.

Housing and Transportation

Housing remains the cornerstone of the high cost of living. With San Francisco’s median home prices consistently ranking among the highest in the nation, mortgage payments, property insurance, and maintenance frequently consume 25% to 35% of a household’s net income. When combined with the cost of maintaining two reliable vehicles, insurance, and fuel, the "middle-class" staples of a home and a car become luxury-priced assets.

The Subjective Nature of Comfort and Modern Lifestyle Expectations

The definition of "living comfortably" has evolved beyond mere survival. In contemporary economic discourse, a comfortable middle-class lifestyle in an expensive city typically includes:

- Ownership of a three-bedroom, two-bathroom home.

- Two late-model vehicles (often one electric or hybrid).

- Annual family vacations (approximately three weeks total).

- The ability to max out retirement accounts (401(k) or IRA).

- Funding for 529 college savings plans.

- Access to quality healthcare and fitness memberships.

Noticeably absent from this list are high-luxury items such as private jets, vacation homes in exclusive resorts, or elite social club memberships. The $408,000 requirement is not for a life of opulence, but for a life of stability and the absence of financial acute stress.

Economic analysts suggest that the rise of remote work has also shifted the "comfort" metric. During the pandemic, many knowledge workers moved away from strict 9-to-5 office schedules. The ability to work from home—or to "quietly quit" by maintaining productivity while reclaiming personal time—has become a form of non-monetary compensation. For some, this freedom is more valuable than a higher salary, leading to a new segment of the population that prioritizes lifestyle flexibility over peak earnings.

Strategic Responses: Geoarbitrage and Income Optimization

For families whose income falls short of the $408,000 threshold, several strategies have emerged to bridge the gap. The most prominent of these is geoarbitrage—the practice of moving to a location with a lower cost of living while maintaining a high income level.

Intra-City and Inter-City Geoarbitrage

Experts recommend a tiered approach to relocation. Rather than immediately moving to a different country, families often find success with "intra-city geoarbitrage." In San Francisco, for example, moving from a high-demand neighborhood like Pacific Heights to a more residential area on the city’s west side can reduce housing costs by as much as 40% while keeping the family within the same social and professional network.

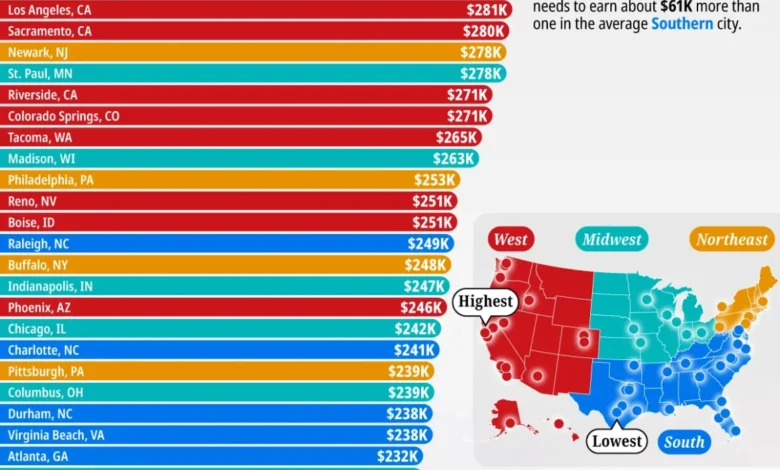

The next tier involves moving to a different city within the same region or state. A move from San Francisco to Honolulu, Hawaii, for instance, can reduce the "comfort" income requirement from $408,000 to $321,000. This $87,000 difference is significant; at a 4% withdrawal rate, a family would need approximately $2.2 million less in total capital to sustain their lifestyle in Hawaii compared to San Francisco. Other cities frequently considered for this strategy include San Diego ($313,000), Los Angeles ($281,000), and Richmond, Virginia ($224,000).

The Sunshine and Lifestyle Premium

Data indicates that families living in Western states generally need to earn $61,000 more on average than those in Southern states to maintain a similar standard of living. This "sunshine premium" accounts for the desirability of Mediterranean climates, proximity to natural beauty, and the robust job markets found in coastal California, Washington, and Oregon.

Implications for Retirement and Long-Term Wealth

An often-overlooked aspect of these high income requirements is that they primarily apply to the "accumulation phase" of life. For those who have already reached retirement, the required income to live comfortably drops significantly. Retirees no longer need to save 20% to 30% of their income for the future, and they are often no longer paying for childcare or education.

For a household that has spent decades earning at the $400,000 level, the transition to retirement can result in a "cash flow shock" in a positive sense. The habit of aggressive saving, once broken, reveals that a comfortable lifestyle can be maintained on a fraction of the previous gross income. Furthermore, the negotiation of severance packages and the utilization of unemployment benefits during career transitions can provide a financial cushion that many workers fail to account for in their long-term planning.

Conclusion: A New Economic Reality

The requirement of a $408,000 annual income to achieve middle-class comfort in San Francisco serves as a stark indicator of the current American economic landscape. It reflects a widening gap between different geographic regions and a fundamental shift in what it costs to secure a stable future for the next generation.

While the figures may seem daunting, they also underscore the importance of proactive financial management. Whether through negotiating higher salaries, optimizing tax efficiency, or deploying geoarbitrage strategies, households are increasingly finding that they must be as strategic about their expenses as they are about their earnings. As inflation continues to influence the cost of essential services, the threshold for "comfort" is likely to remain a moving target, requiring constant adaptation from those residing in the nation’s most expensive urban centers.

{kind=link}